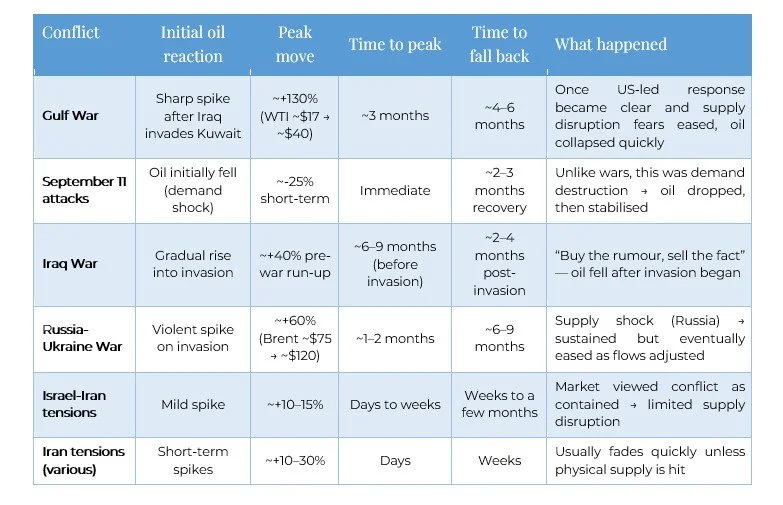

Market Behaviour During Times of Conflict

While history provides useful context, no two market events are ever identical. With that in mind—and acknowledging that views may evolve as new information emerges—our current perspective is as follows:

The likelihood of the Iran conflict being shorter in duration than markets currently expect appears elevated

Oil prices are likely to ease once immediate geopolitical pressures subside

The US is expected to move toward interest rate cuts and potentially expand monetary stimulus, both to support economic growth and assist with any reconstruction-related activity

At present, bond markets are pricing in fewer rate cuts this year, largely due to persistent inflationary pressures—particularly those linked to higher oil prices. This suggests the Federal Reserve may keep rates elevated for longer than previously anticipated.

However, should the conflict prove shorter-lived, a reduction in geopolitical and energy-related pressures could alter this outlook. In that scenario, we may see scope for earlier or more pronounced rate cuts than markets are currently expecting.

Share Market Performance During Periods of Conflict – United States

Looking at historical precedents, a consistent pattern emerges:

Gulf War (1990–1991): The S&P 500 initially fell by around 10% following Iraq’s invasion of Kuwait, before rebounding strongly—rising approximately 20% over the following year

Post-9/11 (2001): Markets declined sharply in the immediate aftermath but recovered within months, gaining around 15% over the next year

Iraq War (2003): A similar pattern played out, with an initial fall followed by a roughly 20% rise over the subsequent 12 months

Russia–Ukraine Conflict (2022): Markets fell between 5–13% in the short term but showed recovery within a year

Israel–Iran Conflict (June 2025): Despite an initial spike in volatility, markets declined by only around 1% and have since recovered to pre-conflict levels

The broader takeaway

Since 1985, US equity markets have demonstrated a high degree of resilience during periods of conflict, typically recovering quickly and delivering positive returns over the medium to longer term (three to ten years).

Key Market Insight

Across most conflicts, market reactions tend to follow a consistent sequence:

Oil prices rise first, driven by fears of supply disruption

The US dollar strengthens, reflecting a flight to safety and liquidity

Gold may lag initially or experience only modest gains

If central banks respond with policy support, gold often becomes a stronger performer later

An Important Exception

In a true financial crisis—such as the Global Financial Crisis—the pattern can differ:

Gold may initially decline due to a liquidity squeeze

This is often followed by a significant rally, supported by quantitative easing and falling interest rates

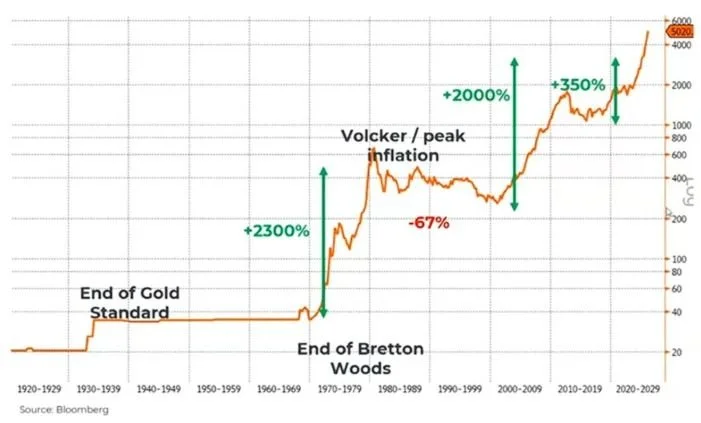

Final Summary

Gold is not typically the first responder in times of conflict — oil is. Instead, gold should be viewed as a second-order play, benefiting from:

Monetary easing

Falling real interest rates

Currency debasement

In most conflicts, gold may rise briefly before stabilising. However, during broader macroeconomic shifts—particularly those involving sustained policy easing—it has the potential to deliver more meaningful and sustained gains.